I wrote the post below a while back and was just about ready to publish it when COVID-19 changed the world . The present crisis brings into focus an aspect of the more theoretical point – there are no players in the field of insurable healthcare who are incentivized and therefore aligned to value and invest in healthy people as a whole. Insurable healthcare is seen primarily as individual responsibility and choice OR as a human right and worthwhile public service. In this system, sick people are a problem that needs to be solved. The only difference in options, to admittedly oversimplify things, is that the right argues the burden ought to be carried by the private sector of individual decisions and market forces, while the left argues that the burden is a worthwhile one to be carried by government obligation, ensuring something like the right to life for all people.

Plenty of individual actors and institutions within the overall system are certainly interested in and greatly value the idea of healthy people. Countless stories have emerged of the heroic efforts doctors, nurses, and others have made to stay ahead of the virus. My point is not to diminish their effectiveness and Herculean efforts but in fact to highlight the extent to which their dedication and sacrifice actually work against or are at least foreign to the outcomes toward which the system of insurable healthcare is aligned. There is no individual, entity, or institution positioned in the current system with the incentive, authority, and desire to even aim at creating a truly healthy populace. In a moment like this, it is only the collective response and health of a nation that are sufficient to overcome such a widespread crisis. But there is no incentive toward collective action within the insurable healthcare system as it currently functions.

On the more practical side of the argument below – especially in the early days of COVID-19, there were stories of people debating whether to get tested or treated because of astronomical costs, even with insurance. To rely on hundreds, if not thousands of individual insurance companies to decide their policies, clearly communicate them to the public, all while the government may or may not impose requirements upon insurers for a financial burden they may or may not be able to handle radically slows response time and leads to much greater costs in terms of life and money. In a crisis like this, it doesn’t actually even matter whether the stories are true at all. People are used to having no idea what anything health related will cost till long after the fact. People will at least hesitate based on those kinds of stories because it is very rational, especially in the beginning of a crisis moment, to assume the odds of any individual being infected are much lower than the odds that they’ll be hit with hundreds or even thousands of dollars in hospital bills they can’t afford.

Without a central player with clear authority to set (or zero out) costs and copays in the midst of a crisis, plenty of people will rationally move much slower toward testing or treatment for fear that their particular insurer may not play by the rules, if any are even set. The government (and essentially the US economy) as that player, is far more highly incentivized, as should be quite evident from recent stock performances, to act quickly than an insurance company that stands only to lose money by making everything free and more widely available to all its customers even if it is the right thing to do. I don’t say that to imply callousness on behalf of insurance companies who are aware of the bottom line even in the midst of a crisis – I say that to highlight the extent to which alignment and incentives define outcomes much more than any individual or even heroic decision made along the way. Especially when every day counts, we need a system that has zero ambiguity as to the financial implications of going to the doctor.

As long as sick people are a problem rather than healthy people being the point, we will never be able to align the power of free market forces in such a way that would prioritize fast response or long term progress toward public health. Single payer insurance at least puts the right pressure on the right player with the right incentives and powers such that the whole system can actually work toward health.

——————————–

Health care in the United States and the corresponding health insurance system are filled with contradictions, problems, and imperfect outcomes despite being one of the most expensive and cutting edge producers of medications and doctors galore. There are far more nuances and problems than I could possibly address here, but I want to offer two reasons that a single payer health insurance plan might cut through some of the stickiest problems of our current system.

More often than not, I see the single payer debate couched in terms like private industry vs socialism or health as individual responsibility vs health as a basic human right. I have no intention of wading into those waters at all. I find the talking points all around to be quite unhelpful or, more to the point, meaningless and undefined. Instead I offer one practical and one theoretical reason why I believe single payer health insurance is at least worth serious consideration.

To express the practical side of the argument I first want to share 5 things I’ve experienced in the process of dealing with health care providers and insurance.

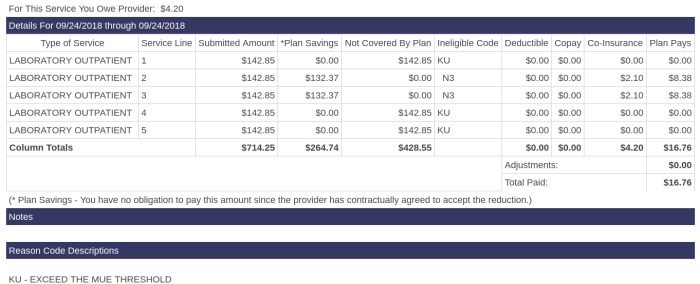

1. At least four or five times, I’ve received bills that look something like this:

The “Submitted amount” column is theoretically the cost of the lab work that was done. “plan savings” represents the discount offered merely because of the deal our insurance company has worked out on our behalf. Two charges show discounts of $132.37 from $142.85. If you can discount your services by more than 90% before anyone pays anything, you are clearly just making up numbers out of thin air.

2. A second issue with the same bill should also be readily apparent. This bill is for 5 tests all ordered at the same time by the same doctor and performed in the same lab on the same visit. Yet two are covered without question and three are not. Those three tests received a code of KU. I fought for a year to figure out what that meant and get it corrected and still have no idea exactly what it means or why it happened. I called both the lab and my insurance no less than 5 times, one time even getting both reps on a conference call together so they could get their act together and make whatever coding changes were needed. I again received a bill asking me to pay the balance with no explanation for what is wrong or what can be done to fix it. My insurance said it wouldn’t pay, the lab said I owed the balance, and I didn’t get any discount on those tests. After the year of fighting, the lab just closed the bill and I didn’t owe anything anymore, no explanation or change ever came.

3. A third issue highlighted by the same bill is the absolute unpredictability of the cost of receiving medical help. After over a year of wrestling over this lab work I still have no idea what I was actually supposed to owe. The idea of knowing cost ahead of time and thereby being able to make informed decisions about where to go or what I can afford is far beyond impossible. On a separate occasion, a medical provider contacted my insurance company to verify coverage and how much my out of pocket cost would be for a particular medical necessity. It was around $200. The provider charged me based on the quote, provided the service, and then officially submitted the claim with my insurance. Over a month after I’d already received the services, I got the final bill. I owed an additional $900 or so. The provider said the initial bill was only an estimate and no guarantee. Insurance said they don’t quote figures ahead of time. Even when health costs are supposedly confirmed beforehand, they can be completely arbitrary numbers with zero relationship to reality.

4. A final problem with this specific bill is the three categories to the right that indicate how much I owe – deductible, copay, and coinsurance. These are 3 different types of payments my insurance company expects me to make. I have no problem with the theory that these types of breakdowns would exist. The problem is that it is never entirely clear which categories will be affected for which types of services and visits. These categories unnecessarily obfuscate the amount that will be paid for any particular health service, even assuming the bottom line cost is in any way reflective of reality.

5. Separately from all that, I previously dealt with another absurd consequence of our insurance and billing weirdness. I was billed for a dozen or so of the same type of visits to the same doctor for the same health concern over the course of a few months. Every bill required a copay of $30 or so. But two of the visits also came with a $300 or so ‘hospital room use’ fee. There was no explanation as to why these fees applied to only these 2 visits, but my insurance company denied the charges because they said there were coding issues and the hospital sent me numerous bills. The doctor said they couldn’t change the code, the insurance said they couldn’t accept the code, and the hospital said I owed the money. After more than a year of asking questions, I finally spoke with a hospital higher up who is in charge of customer relations. I explained the situation yet again and he came back a while later and offered to give me a 90% reduction and we’d call it even. I’d owe something like $60 and we’d all walk away happy. I said I’d gladly pay the $600 if someone could just tell me why I was being charged for these 2 visits and no others, but I would not pay a penny until someone had answers. A couple of weeks later, he called back and the bills had been closed – again with no explanation and no change in the stance of my doctor or insurance company.

Each of these anecdotes is only possible within a system that both complicates the relationship between providers, customers, and insurers and obfuscates every cost involved to the point that no one can make a rational decision about anything in the process. To whittle insurance down to a single payer for everyone in the system does not solve every problem, but it at least makes it possible to know and understand the game that we are all playing. At most, any test or procedure or appointment would only have 2 possible costs – full price and insured price. There would not be 1000 different contracts with 1000 different companies that allow providers to make up numbers that have no relationship to reality. With only a provider, one consistent insurer, and the patient involved, it would take infinitely less effort to lay out clear and consistent expectations for who charges/pays what and who may be at fault when problems arise.

———————————————–

To express the theoretical side of the argument, I need to offer a brief word on the power of alignment. In companies, different markets and business models lend themselves to different ways of structuring employees, setting up incentives, and a variety of other core decisions necessary to run a successful business.

A common and fairly simple way to illustrate the importance of alignment is in the difference between a company like Google and one like Apple. Google makes almost all of its profits on advertising, whereas Apple makes its profits from products (most from the iPhone). That difference incentivizes Google to ensure that everyone, everywhere is using Google’s services. More users means more eyeballs, which means more advertising dollars. Apple, on the other hand, makes money from high end computer products with high profit margins. Thus, Apple necessarily limits its addressable market and allows lower cost phones and computers to cannibalize each other. Apple also artificially limits services to its own hardware to increase customer lock in (such as iMessage).

Google’s entire business alignment lends itself to pushing products out the door and iterating quickly through software, which helps explain why they have struggled to make a dent in the hardware space in which a company must sell a mostly final product and can only do so much through software updates. Apple is better than almost any other company at pushing out great hardware, which helps explain why they have struggled to create necessarily iterative and unfinished services like maps or Siri that can match the capabilities of Google or Amazon. Everything down to the decision to have only one profit and loss statement as a company aligns every aspect of the business toward selling specific hardware.

Neither business model or market approach is better or worse as should be evident by the presence of both companies at or near the top of the stock market for quite some time now. They are, however, aligned to run based on very different goals and incentives.

Which brings us back to healthcare.

In our current system, insurers are aligned to extract the most money from patients while paying the least to healthcare providers. Insurers, on one hand, must keep patients from getting so much more unhealthy than the patients of their competitors that someone with the power to do something might act. Add in the fact that employers often choose insurance companies rather than direct consumers and there is usually almost no correlation between patient experience and pressure on insurance companies to change. No insurer has any reason other than a vague sense of good will to do more than triaging the worst health conditions (as opposed to offering proactive and sustainable health initiatives beyond a handful of highly cost effective preventative measures like free flu shots). On the other hand, the more likely someone is to be ill, the more likely they are to purchase insurance and vice versa. Profitability for insurance relies on having a great enough number of people involved such that overall risk and costs are predictable even though any particular individual may require nothing and another may require millions of dollars in care. Pushed to the logical extreme, if insurance made people completely healthy, the insurance market would put itself out of business. These two realities are not meant to imply that insurance companies do anything nefarious or wrong in the choices they make – they instead point out that the business model of insurance is deeply incentivized to maintain sick, but not critically ill people. Alignment is not around making healthy people but around profiting off of every individual’s rational concern that one illness could lead to bankruptcy without insurance. Insurance companies do a lot of good, but doing more than the absolute minimum is often actually against the business interests of the companies.

Providers operate with the same lack of incentive to make people completely healthy because profitability comes through addressing specific illnesses, not sustaining health. Additionally, providers are incentivized to extract as much money from patients and insurers as possible. Providers have every reason to push costs as high as possible knowing the bulk of payment won’t come from the patient who is making acute decisions, the patient can’t know much about the level of necessity for treatment much less it’s cost when making decisions, many patients are told where to go by their insurers anyway, and the billing process is so opaque and complicated that only the most diligent and intelligent patients can even figure out what they should have truly paid.

Patients are incentivized at least to not die and perhaps to attain some level of health while spending as little as possible. Any patient with an expensive health concern, most commonly diabetes, is often forced to choose between potentially bankrupting themselves or taking the medicine they need to remain stable. Individuals may or may not take necessary steps towards health but staying well for any individual is always a matter of luck as much as it is a matter of personal choices. Individuals also lack the robust information necessary to make the best possible choices.

To align health insurance around a single payer government model makes it possible to align incentives toward insurance as an investment in a nation’s greatest asset – the health of its people. Having more healthy people who are able to focus on anything other than their health and its financial impact on their lives frees up an enormous amount of potential for the growth of all other economic sectors. Knowing the bulk of the healthcare cost rests in the government finally gives someone with a financial stake in the outcome an incentive to understand what causes negative health outcomes and what policies can be adopted for long term financial and physical health. It also places much of the cost of un-health on the only player (the government) that has the broad reaching powers to structure policies, laws, and other incentives toward a healthier society.

With a system set up to invest in people, providers would then be able to offer specific rates for service ahead of time and know with much greater certainty what will be covered and how. The government could (as it already does to some extent) determine what aspects of covered healthcare are essential for creating healthier people and allow providers to build ancillary benefits around which to differentiate their services and costs. The provider market would finally have some semblance of direct market forces guiding its decisions, the government as insurer would be capable of incorporating healthy people as an essential principle rather than accidental outcome of profit, and patients would be able to make real and meaningful decisions about their health and wealth.

Properly aligned incentives don’t solve nearly every problem with the healthcare system in the US. But alignment is a primary factor defining culture and decision making over time. Alignment and the interrelated incentives and cultures that flow from alignment do more to determine outcomes than anything else in a system. The structure of our current system is a muddled mess in which no one besides an individual patient has any incentive to work towards actual health. Aligning the system around a single payer would at least make it possible for that system to be directed toward healthy people rather than simply fighting illness.